How Much Is My Mortgage Note Worth?

A mortgage note can feel simple when payments are coming in every month.

A buyer sends you a check. You deposit it. The note balance slowly goes down. On paper, it looks like dependable income.

Then life changes.

Maybe you inherited the note. Maybe you need cash for retirement, medical bills, taxes, debt payoff, a business opportunity, or a family situation. Maybe the borrower is paying late. Maybe you simply want to know your mortgage note value before deciding whether to keep it or sell it.

That is when most note holders ask the same question:

How much is my mortgage note worth?

The honest answer is… it depends:

Your mortgage note is usually worth less than the unpaid balance, but it may still be worth a substantial amount of cash depending on the payment history, interest rate, property value, borrower strength, note terms, documentation, and current investor yield requirements. For context check out Current Freddie Mac Interest rates.

At American Funding Group, we have purchased thousands of private mortgage notes, deeds of trust, land contracts, and seller-financed real estate notes over more than three decades. We evaluate both full note purchases and partial mortgage note sales, which means you may not have to sell your entire note to get the cash you need.

📞 Call (772) 232-2383 or Get My Note Quote Now

How much Is My Mortgage Note Worth?

Mortgage Note value is based on the present value of its future payments, adjusted for risk.

That sounds technical, but the idea is simple.

A note buyer is not only buying the unpaid balance. The buyer is purchasing the right to receive future payments. Those payments are worth more when they are predictable, well-documented, secured by strong real estate, and supported by a borrower with a good payment history.

They are worth less when the note has risk.

For example, two notes may both have a $100,000 unpaid balance, but they may not be worth the same amount.

A note with:

- On-time payments

- Strong borrower credit

- Good property equity

- A market interest rate

- Complete documents

- A first lien position

will usually receive a stronger offer than a note with:

- Late payments

- Missing documents

- Weak borrower credit

- Low equity

- A low interest rate

- A second lien position

- Unpaid taxes or insurance problems

This is why online “mortgage note calculators” can be misleading. They may estimate value based on balance, rate, and term, but they often miss the real-world details that drive pricing.

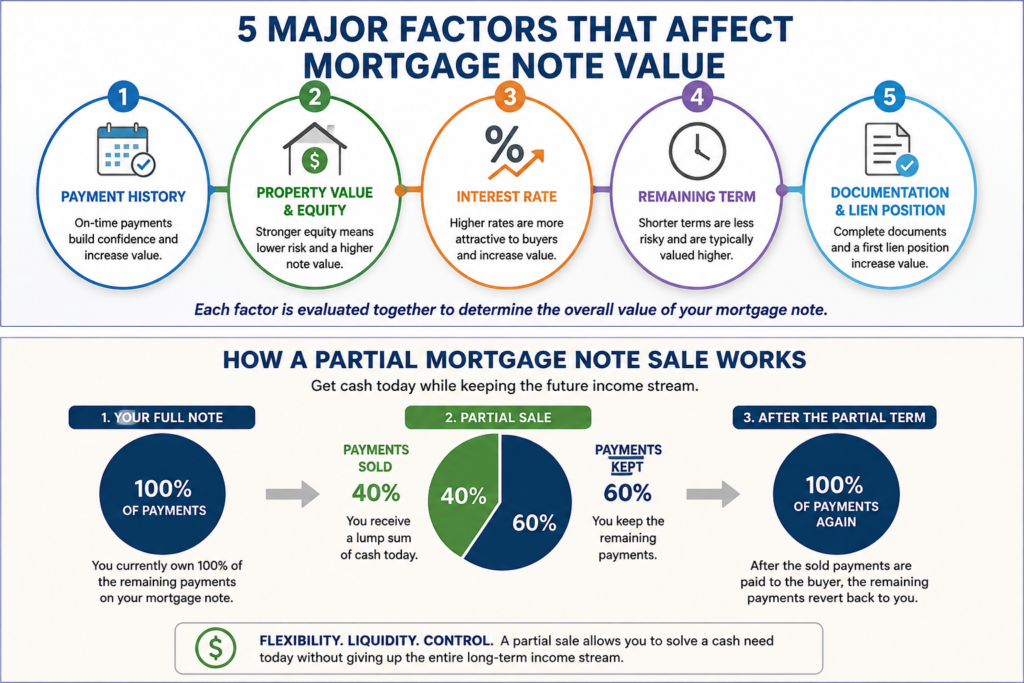

The Most Important Factors That Affect Mortgage Note Value

1. Payment History

Payment history is one of the strongest indicators of note value.

A borrower who has paid on time for years creates confidence. A borrower who pays late, misses payments, or only pays when pressured creates uncertainty.

A note buyer will usually ask:

- How many payments have been made?

- Were payments made on time?

- Are there any missed payments?

- Is there a written payment history?

- Are payments made through a servicing company or directly to the seller?

A seasoned note with 24 months of clean payment history is usually stronger than a brand-new note with only one or two payments made.

2. Property Value and Equity

The property securing the note matters because it protects the investment.

A buyer will look at the relationship between the property value and the unpaid loan balance. This is often called the loan-to-value ratio.

If the property is worth $200,000 and the note balance is $100,000, there is a strong equity cushion. If the property is worth $110,000 and the note balance is $100,000, the risk is much higher.

More equity usually means a stronger note value.

Less equity usually means a larger discount.

3. Interest Rate on the Note

The interest rate on your note affects its market value. See the FRED mortgage-rate chart for historical rate context

If your note has a 8% interest rate, it should be more attractive than a note with a 3% interest rate, assuming the other facts are similar.

This is especially important in a higher-rate environment. When current mortgage rates are above many older seller-financed note rates, investors may require a discount to make a low-rate note attractive.

A low interest rate does not mean your note cannot be sold. It means the buyer may price the note at a larger discount to reach an acceptable yield.

4. Remaining Term

The remaining term affects how long the buyer must wait to receive the payments.

A note with 5 years remaining is very different from a note with 25 years remaining.

Longer notes may produce more total payments, but they also expose the buyer to more long-term uncertainty. Shorter notes may be easier to value because the repayment period is more predictable.

5. Down Payment and Borrower Equity

The original down payment matters.

A borrower who put down 20%, 30%, or more usually has more financial commitment to the property. A borrower who put down very little may have less incentive to continue to make payments if problems arise.

Large down payments often support stronger pricing as they demonstrate that the borrower has “more skin in the game.”

Small down payments can reduce your note sales value, especially if the note is new or the borrower has weak credit.

6. Borrower Credit and Stability

Private mortgage notes are often created because the buyer could not or did not want to use traditional bank financing.

That does not automatically make the note bad.

But borrower strength matters.

In determining Mortgage Note value, a buyer will review:

- Credit score

- Payment history

- Bankruptcy history

- Prior mortgage history

- Overall ability to pay

A strong borrower will improve pricing. A weak borrower may reduce the offer.

7. First Position vs. Second Position

A first mortgage or first deed of trust is always more valuable than a second lien. Why?

Because the first lien holder has priority if the borrower defaults and the property must be foreclosed.

Second liens can still be sold, but they carry more risk. If there is not enough equity in the property, a second lien may have limited protection.

8. Type and Condition of Property

The collateral matters.

Notes secured by owner-occupied single-family homes are often easier to sell than notes secured by unusual, distressed, or highly specialized property.

Property types that may affect value include:

- Single-family homes

- Condos

- Townhomes

- Multifamily properties

- Commercial buildings

- Land

- Mobile or manufactured homes

- Rural property

- Mixed-use property

A well-maintained home in a strong market usually supports better pricing than a distressed property in a weak or difficult-to-sell location.

9. Documentation

Documentation can make or break a note sale.

A strong file will include:

- Promissory note

- Mortgage, deed of trust, land contract, or security instrument

- Closing statement

- Payment history

- Title policy

- Property insurance information

- Borrower contact information

- Servicing records

- Assignment history, if applicable

Missing documents do not always kill a deal, but they can slow the process or reduce value.

At American Funding Group, we help note holders work through documentation problems as many private notes are not perfectly organized.

10. Current Investor Yield Requirements

This is the factor many note holders never see.

A note buyer is comparing your note to other investment opportunities. If market rates rise, investors often require a higher yield. resulting in a lower note sale price.I

That is why the same note may receive a different offer today than it would have received several years ago.

Why Your Note Is Usually Worth Less Than the Unpaid Balance

Many note holders assume a $100,000 note should sell for $100,000.

Usually, it does not.

The buyer is taking on:

- Default risk

- Time risk

- Interest rate risk

- Property value risk

- Documentation risk

- Legal and closing costs

- Servicing and collection responsibility

The buyer also needs a return on investment.

That return is created by purchasing the note at a discount.

This does not mean the offer is unfair. It means the buyer is pricing the future income stream based on risk and yield.

Example: Why Two $100,000 Notes Can Have Very Different Values

Note A

- $100,000 unpaid balance

- 8% interest rate

- 120 payments remaining

- 24 months of on-time payments

- First lien

- Property worth $200,000

- Strong borrower

- Complete documents

This note may receive a strong offer because the risk is relatively low.

Note B

- $100,000 unpaid balance

- 3% interest rate

- 300 payments remaining

- Borrower has paid late several times

- Property worth $125,000

- Missing title policy

- Weak borrower credit

- Unpaid property taxes

This note will still have value, but the offer will be lower because the buyer is taking on more risk.

The unpaid balance is the same, but the value is not.

Can I Sell Part of My Mortgage Note Instead of the Entire Note?

Yes. This is one of the most overlooked options in the note business.

A partial mortgage note sale allows you to sell only a portion of the future payments while keeping the rest of the note.

For many note holders, this can be a better solution than selling the entire note.

Instead of asking: “How much can I get if I sell my whole note?”…

You may want to ask yourself… how much cash do I need right now? Can I sell only enough payments to meet that need?”

How a Partial Note Sale Works

Assume you receive monthly payments from a borrower. With a partial sale, you may sell:

- The next 60 payments

- The next 84 payments

- A specific dollar amount of future payments

- A split structure where the buyer receives payments for a set period and then the note reverts back to you

After the buyer receives the agreed payments, the remaining payments go back to you.

This can be powerful because you receive a lump sum today without giving up the entire long-term income stream.

Example of a Partial Mortgage Note Sale

Suppose your note has:

- $150,000 unpaid balance

- $1,400 monthly payment

- 180 payments remaining

You need $50,000 now.

Instead of selling the entire note, you may be able to sell a set number of future payments to generate the cash you need.

You receive a lump sum now. The note buyer receives the agreed payment stream. After that partial term ends, the remaining payments come back to you.

This can help you solve a short-term cash need while preserving long-term value.

When a Partial Sale May Be Better Than a Full Sale

A partial sale may be worth considering when:

- You do not need all the cash at once

- You want to keep some future income

- You believe the borrower will continue paying

- You want to reduce risk but not eliminate the note completely

- You need money for taxes, debt, repairs, retirement, or a family issue

- You want liquidity without giving up the entire asset

Many note holders do not know partial sales exist until they speak with an experienced note buyer.

That is why American Funding Group evaluates both full and partial purchase options.

When a Full Sale May Be Better

A full sale may make more sense when:

- You want to be completely done with the note

- The borrower is becoming difficult

- You inherited the note and do not want to manage it

- You are going through divorce or estate settlement

- You need maximum cash now

- You are concerned about future default

- You want to move money into another investment

There is no universal right answer. The best structure depends on your goals.

The Hidden Question: Do You Want Maximum Cash or the Best Overall Outcome?

Many note holders ask for the highest possible offer.

That is understandable.

But the better question is:

“What structure gives me the best overall result?”

Sometimes the best result is a full mortgage note sale.

Sometimes the best result is a partial mortgage note sale.

Sometimes the best result is holding the note.

A reputable note buyer should explain your options clearly instead of pressuring you into one solution.

At American Funding Group, the goal is not just to quote a number. The goal is to understand the note, the property, the borrower, and your reason for considering a sale.

Info needed to find out how much is my mortgage note worth

To estimate your mortgage note value, gather as much of the following as possible:

- Current unpaid balance

- Monthly payment amount

- Interest rate

- Remaining term

- Original sale price

- Original down payment

- Property address

- Type of property

- Borrower name(s)

- Borrower payment history

- Copy of the note

- Copy of the mortgage, deed of trust, or land contract

- Property tax status

- Insurance status

- Whether the note is serviced by a third party

Do not worry if you are missing something.

Many note holders do not have a perfect file. An experienced buyer can usually tell you what is essential and what can be recreated, verified, or worked around.

Common Reasons People Sell Mortgage Notes

People sell mortgage notes for many reasons, including:

- Retirement planning

- Medical expenses

- Paying off debt

- Buying another property

- Settling an estate

- Divorce

- Business capital

- Helping family

- Reducing collection headaches

- Concern about borrower default

- Simplifying finances

The reason matters because it may affect whether a full sale or partial sale is better.

For example, someone who needs a specific amount of cash may be a good partial-sale candidate. Someone who wants to eliminate future responsibility may prefer a full sale.

Does a Mortgage Note Buyer Pay the Same Amount as a Bank?

Usually, no.

Private mortgage notes are different from institutional bank loans.

A bank loan is typically meticulously underwritten before closing…using formal credit, income, appraisal, and compliance standards. Private seller-financed notes are created more informally.

That does not make them bad. It means the buyer must evaluate the note carefully and price the risk.

What Makes American Funding Group Different?

American Funding Group has been buying private mortgage notes for more than three decades.

We buy:

- Seller-financed mortgage notes

- Deeds of trust

- Land contracts

- Contracts for deed

- Private real estate notes

- Performing notes

- Problem notes

- Full notes

- Partial notes

We work with note holders nationwide and have experience with straightforward notes as well as more complicated situations involving late payments, missing documents, inherited notes, divorce, probate, and unusual collateral.

Our job is to help you understand your options clearly.

You may discover that selling the full note is best.

You may discover that a partial sale gives you the cash you need while preserving future income.

Or you may decide to keep the note.

Either way, the first step is understanding what your mortgage note is worth.

Frequently Asked Questions

How much can I sell my mortgage note for?

The value depends on the unpaid balance, payment amount, interest rate, remaining term, borrower payment history, property value, equity, lien position, documentation, and current investor yield requirements. Most mortgage notes sell at a discount to the unpaid balance.

Can I sell only part of my mortgage note?

Yes. A partial note sale allows you to sell a portion of future payments while keeping the remaining payments after the partial term ends.

Why is my note worth less than the balance?

Your note is worth less than the balance because the buyer is purchasing future payments and assuming risk. The buyer must account for default risk, time, property value, interest rates, servicing, and required investment return.

What is the most important factor in note value?

Payment history, property equity, borrower credit performance and documentation are among the most important factors. A well-documented note with a strong payment history and good equity usually receives a better offer.

Can I sell a note if the borrower has been late?

Yes, but late payments can reduce the value. American Funding Group reviews problem notes and may still be able to provide an offer.

Do I need perfect documents to sell my note?

Not always. Complete documents help, but many private note files have issues. An experienced note buyer can review what you have and explain what may be needed.

Is a partial note sale better than a full sale?

It depends on your goals. A partial sale may be better if you need a specific amount of cash but want to keep future income. A full sale may be better if you want maximum cash now or want to eliminate future responsibility.

How long does it take to sell a mortgage note?

Timing depends on documentation, title review, property information, and borrower/payment verification. Many note sales can close in a few weeks once the necessary information is reviewed.

Final Thought: Your Note May Have More Options Than You Think

If you are asking, “How much is my mortgage note worth?” you may be closer to a solution than you realize.

The answer is not just a number.

It is a strategy.

You may be able to sell the entire note. You may be able to sell part of the note. You may be able to use the note to solve a short-term cash need while still keeping long-term income.

The best way to find out is to have the note reviewed by an experienced buyer who understands both full purchases and partial note sales.

American Funding Group has helped note holders nationwide evaluate and sell private mortgage notes for more than 30 years.

If you want to know what your mortgage note is worth, we can review the details and explain your optio