How to sell a Promissory Note… Who buys Promissory Notes?

A Promissory Note often starts as a smart solution.

Maybe you sold a property and agreed to let the buyer pay you over time. Maybe you helped a family member, sold a business, or accepted payments because traditional bank financing was not available. At first, the monthly income felt useful. It created steady cash flow, interest income, and flexibility.

Then life changed.

You may now need cash for retirement, medical expenses, debt payoff, another investment, estate settlement, divorce, taxes, or simply peace of mind. That is when many note holders ask the same two questions:

Can I sell my promissory note? Who buys promissory notes?

The answer is yes — many promissory notes can be sold. But the amount a buyer will pay depends on the note type, payment history, documentation, collateral, borrower strength, and risk.

American Funding Group has been buying private mortgage notes, land contracts, deeds of trust, and real estate-secured promissory notes for over 30 years. We help note holders understand their options clearly, including full purchases, partial purchases, and creative solutions for notes with problems.

What Is a Promissory Note?

A promissory note is a written promise to repay money under specific terms. It usually identifies:

- The borrower

- The lender or note holder

- The original loan amount

- The interest rate

- The payment amount

- The payment schedule

- The maturity date

- Late charges or default terms

In real estate transactions, the promissory note is often paired with a mortgage, deed of trust, land contract, contract for deed, or other security document. The note is the borrower’s promise to pay. The mortgage or deed of trust is what secures that promise against the property.

Can You Sell a Promissory Note?

Yes. A promissory note can often be sold to a private investor, note investment company, institutional note buyer, or specialized mortgage note buyer.

This distinction matters. An unsecured promissory note will be harder to sell. A real estate-secured promissory note is more attractive because the buyer has collateral backing the payments.

When you sell a note, you are selling the right to receive future payments. Instead of collecting payments monthly over many years, you receive a lump sum now.

For example, if your buyer owes you $150,000 payable over 15 years, a note buyer may purchase all or part of those future payments. You receive cash now, and the buyer receives the future income stream.

The buyer does not pay the full remaining balance dollar-for-dollar. The note is purchased at a discount because the buyer is taking on risk, waiting for future payments, and tying up capital.

Who Buys Promissory Notes?

Promissory notes are typically purchased by:

- Private mortgage note buyers

These buyers specialize in real estate-secured notes, including seller-financed mortgages, deeds of trust, land contracts, and contracts for deed. - Institutional note investors

These are larger companies or funding sources that buy notes as investment assets. - Private investors

Some individuals buy notes for income, but they may be selective and may not handle complex files. - Note brokers

Brokers do not always buy the note themselves. They may shop the note to investors and earn a fee or spread. - Specialized companies like American Funding Group

American Funding Group works directly with note holders and has decades of experience evaluating private mortgage notes, including notes that may not fit a simple “perfect note” formula.

If the property securing your note is located in Florida, see our guide to Florida Note Buyers. Property owners in Texas can also review our Texas Mortgage Note Buyers guide. Michigan note holders can learn more on our Michigan Note Buyers page.

📞 Call (772) 232-2383 or Get My Note Quote Now

Why People Sell Promissory Notes

Most note holders do not sell because the note is bad. They sell because their needs changed.

Common reasons include:

- Paying off debt

- Retirement planning

- Settling an estate

- Medical expenses

- Buying another property

- Helping family

- Avoiding years of collection responsibility

- Removing uncertainty

- Reinvesting into something more useful

- Reducing exposure to borrower default

- Many heirs inherit promissory notes through estates and probate proceedings. Learn how to sell an inherited mortgage note.

- Divorce settlements frequently create situations where one party wants to convert a note into immediate cash. Learn more about how to sell a mortgage note after divorce.

A note may look good on paper, but future payments are not the same as cash in hand. Selling converts an uncertain stream of future payments into immediate liquidity.

The Hidden Issue: A Note Is Not Just a Balance

Many sellers focus on the unpaid balance. That is understandable, but buyers look deeper.

A $200,000 note is not automatically worth $200,000 today.

A buyer studies the note like an income-producing asset. The real question is:

How safe, documented, enforceable, and predictable are the future payments?

That is why two notes with the same unpaid balance can receive very different offers.

A note with strong equity, seasoned payments, complete documents, and a reliable payer will usually bring a stronger offer. A note with missing paperwork, poor payment history, low equity, or unclear servicing may still be sellable, but it will usually be discounted more heavily.

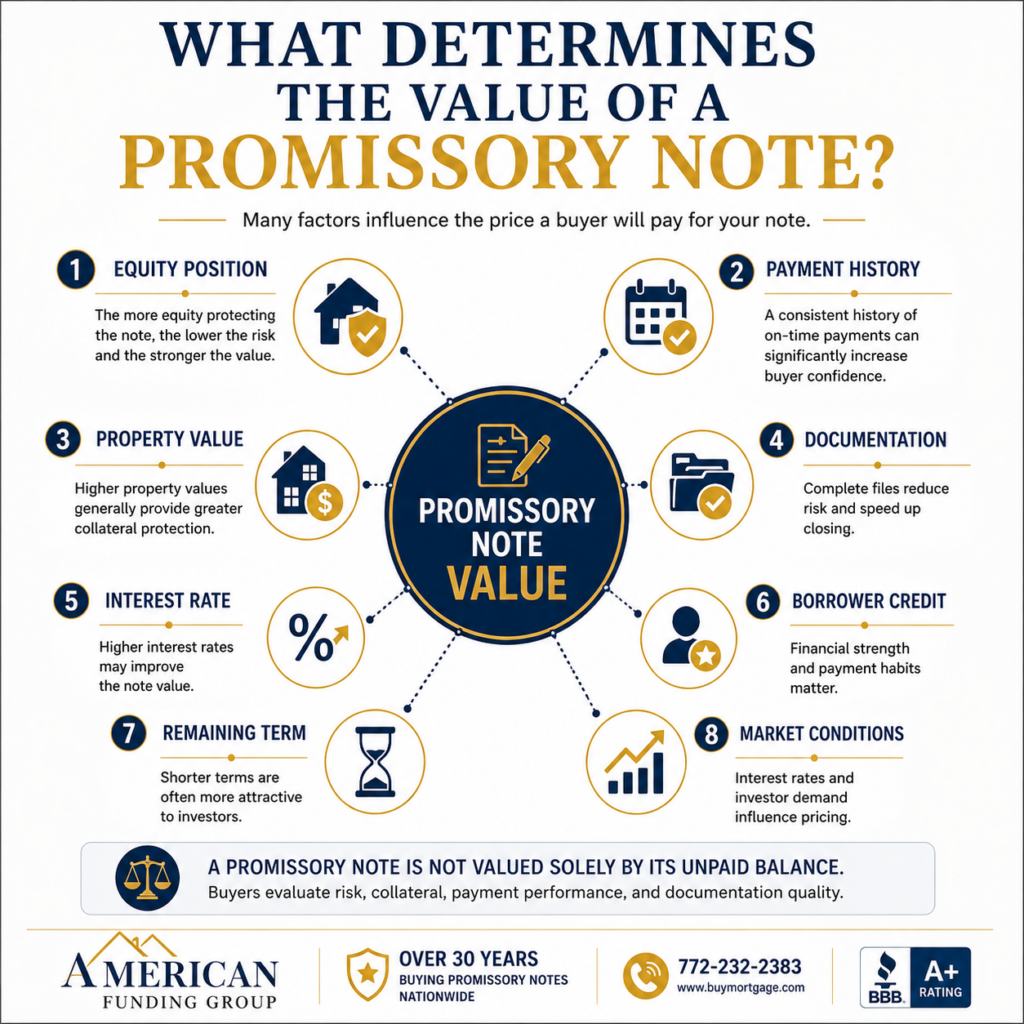

What Affects the Value of a Promissory Note?

1. Type of Collateral

Several factors determine what a promissory note buyer may pay.

A real estate-secured note is usually more valuable than an unsecured note. A note secured by a residential property, commercial building, or land gives the buyer more protection than a personal IOU.

2. Property Value and Equity

Equity is one of the biggest value drivers. If the property is worth much more than the note balance, the buyer has a stronger safety cushion.

For example, a $100,000 note secured by a property worth $200,000 is usually more attractive than a $100,000 note secured by a property worth $110,000.

3. Payment History

A clean payment history builds confidence. Buyers like to see that the payer has made payments on time for at least several months.

A brand-new note can still be sold, but a seasoned note often receives better pricing.

4. Interest Rate

A higher interest rate may increase value because the buyer receives a stronger return. A very low interest rate may reduce value, especially when current market rates are higher.

5. Down Payment

The original buyer’s down payment matters. A larger down payment usually means the payer has more money invested and is less likely to walk away.

6. Documentation

Complete paperwork can increase buyer confidence. Important documents may include:

- Promissory note

- Mortgage or deed of trust

- Closing statement

- Payment history

- Buyer information

- Property insurance details

- Tax status

- Title documents

- Land contract or contract for deed, if applicable

7. Borrower Credit and Stability

A buyer may consider the payer’s credit, employment, payment behavior, and overall reliability.

8. Remaining Term

A note with payments spread over many years may be discounted more because the buyer must wait longer to recover the investment.

9. Legal and Servicing Issues

Problems such as missing assignments, unpaid taxes, poor servicing records, unclear ownership, or late payments can affect pricing.

Full Sale vs. Partial Sale

Many note holders assume they must sell the entire note. That is not always true.

You may be able to sell:

- The entire note

- A specific number of future payments

- A partial interest

- A balloon payment

- A portion of the remaining balance

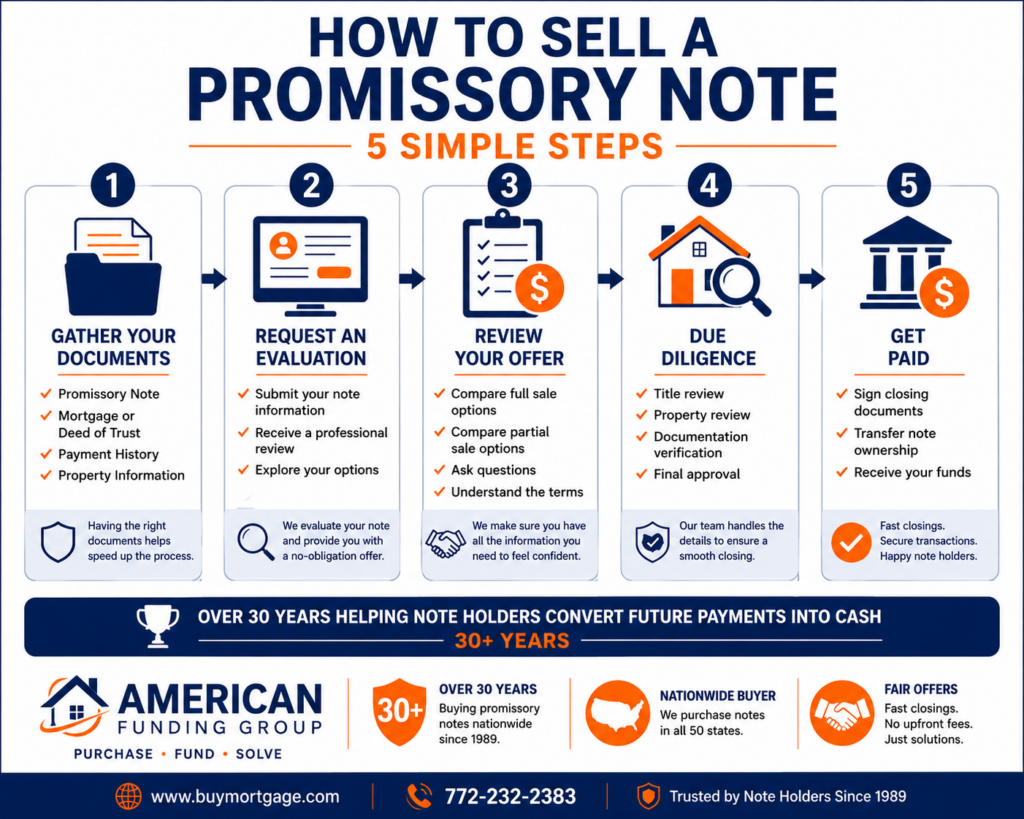

How to Sell a Promissory Note

Step 1: Gather Your Documents

A partial sale can be useful when you need cash now but still want to keep some future income.

For example, instead of selling a 15-year note completely, you might sell the next 60 monthly payments. After that period, the remaining payments may return to you.

This is one of the most overlooked strategies in the note business. A partial sale can sometimes produce the cash you need while preserving long-term value.

Start with the promissory note and any security instrument, such as a mortgage, deed of trust, land contract, or contract for deed.

Also gather the payment history, property address, insurance information, tax status, and closing documents.

Step 2: Request a Note Evaluation

A note buyer will review the terms, payment history, collateral, property value, and documentation.

American Funding Group can evaluate many types of real estate-secured notes, including notes with unusual terms or problems.

Step 3: Review Your Options

You may receive options for a full purchase, partial purchase, or other structure.

The highest offer is not always the best offer if it comes with unclear terms, junk fees, delays, or bait-and-switch tactics.

Step 4: Due Diligence

The buyer may verify the property value, title, taxes, insurance, payment history, and borrower details.

Step 5: Closing and Assignment

If you accept the offer, the transaction is documented. The note and related security documents are assigned to the buyer. You receive your funds at closing.

Do You Have to Sell the Whole Note?

No. In many cases, you can sell part of the note.

This matters because some note holders only need a specific amount of cash. Selling the whole note may create more liquidity than necessary while giving up all future payments.

A partial purchase may be a better fit when:

- You need cash now

- You still want future income

- The note has strong long-term value

- You want flexibility

- You are planning for retirement or estate needs

American Funding Group can explain whether a partial sale makes sense based on your note.

📞 Call (772) 232-2383 or Get My Note Quote Now

Can You Sell a Problem Promissory Note?

Sometimes, yes.

A problem note may still have value if it is secured by real estate and the documents can be reviewed. Common issues include:

- Late payments

- Missing payment records

- Low interest rate

- Poor borrower credit

- Balloon payment concerns

- Divorce-related ownership questions

- Probate or estate complications

- Unpaid taxes

- Incomplete documentation

- Land contract issues

- Non-performing payments

Some buyers only want clean, performing notes. American Funding Group has experience with more complicated situations and can often identify options other buyers overlook.

How Much Is My Promissory Note Worth?

A note’s value is based on risk and return.

A buyer will usually discount the remaining balance to account for:

- Time value of money

- Default risk

- Property risk

- Documentation risk

- Servicing risk

- Legal risk

- Market interest rates

- Cost of capital

This is why online calculators often give misleading results. They may estimate value using interest rate and balance, but they cannot fully measure documentation quality, collateral risk, payer behavior, or legal issues.

The best way to know what your note is worth is to have it reviewed by an experienced note buyer.

Promissory Note Buyers vs. Brokers

Not everyone advertising “we buy notes” is the actual buyer.

A direct note buyer uses its own capital or direct funding relationships to purchase notes. A broker may simply shop your note to multiple buyers.

Working with a broker is not always bad, but it can create confusion if you do not know who is actually funding the purchase.

Before choosing a company, ask:

- Are you the buyer or a broker?

- Are there any upfront fees?

- Who pays closing costs?

- How long does closing usually take?

- Will the offer change after due diligence?

- What documents do you need?

- Can you buy partial notes?

- Do you handle problem notes?

A reputable buyer should explain the process clearly and should not pressure you into a rushed decision.

Why American Funding Group

American Funding Group has been buying private mortgage notes and real estate-secured promissory notes for over three decades.

We buy many types of notes, including:

- Seller-financed mortgage notes

- Promissory notes secured by real estate

- Deeds of trust

- Land contracts

- Contracts for deed

- Commercial notes

- Residential notes

- Performing and non-performing notes

- Full and partial notes

Our strength is not just making offers. It is understanding the story behind the note.

Some notes are simple. Others involve divorce, probate, missing documents, late payments, unclear title issues, or unusual property types. Experience matters because small details can make a major difference in whether a note can be purchased and how the transaction should be structured.

American Funding Group treats note holders with respect, explains options clearly, and looks for practical solutions instead of one-size-fits-all answers.

What Documents Help You Get a Better Offer?

You do not need to have everything perfect before asking for an evaluation, but the more complete your file is, the easier it is to receive a serious offer.

Helpful documents include:

- Copy of the promissory note

- Mortgage, deed of trust, land contract, or contract for deed

- Settlement statement or closing statement

- Current unpaid balance

- Payment history

- Property address

- Borrower contact information

- Proof of insurance

- Property tax information

- Title policy, if available

- Appraisal or recent value estimate, if available

Good documentation reduces uncertainty. Lower uncertainty can support stronger pricing.

Common Mistakes When Selling a Promissory Note

Mistake 1: Only Comparing the Top Number

A high verbal offer means little if it changes later. Look for clarity, reliability, and experience.

Mistake 2: Assuming Every Buyer Understands Problem Notes

Some buyers only want clean files. If your note has complications, work with someone who understands them.

Mistake 3: Not Considering a Partial Sale

A full sale is not the only option. A partial may solve your cash need while preserving future income.

Mistake 4: Waiting Until the Note Becomes Distressed

If payments are current, your note may be more attractive. Waiting until the payer defaults can reduce value.

Mistake 5: Poor Recordkeeping

Keep payment records, insurance information, tax status, and borrower correspondence organized.

Related Resources:

Frequently Asked Questions

Can I sell my promissory note?

Yes, many promissory notes can be sold, especially if they are secured by real estate. The value depends on the note terms, collateral, payment history, and documentation.

Who buys promissory notes?

Promissory notes are bought by private investors, note buying companies, institutional investors, and specialized real estate note buyers such as American Funding Group.

Can I sell part of my promissory note?

Yes. Many note holders sell only a portion of their future payments. This is called a partial note sale.

How long does it take to sell a promissory note?

Timing depends on the complexity of the file, title review, documentation, and due diligence. A clean real estate-secured note can often move faster than a note with missing documents or legal issues.

Do promissory note buyers pay the full balance?

Usually no. Notes are generally purchased at a discount because the buyer is taking on risk and waiting for future payments.

Can I sell a note if the payer is late?

Possibly. Late payments may reduce value, but a real estate-secured note may still have value.

What if I lost some documents?

You may still have options. American Funding Group can review what you have and explain what may be needed.

Is selling a promissory note taxable?

Selling a note may have tax consequences. You should speak with a qualified tax professional before making a final decision.

Final Thoughts

Selling a promissory note is not just about finding someone willing to buy payments. It is about understanding what you own, what makes it valuable, and what structure best fits your needs.

A strong note may provide a clean path to cash. A complicated note may still have value if reviewed by an experienced buyer. A partial sale may give you liquidity without giving up the entire income stream.

If you are asking, “How do I sell my promissory note?” or “Who buys promissory notes?” American Funding Group can help you evaluate your options clearly and respectfully.

For over 30 years, American Funding Group has helped note holders turn future payments into practical cash solutions.

Call American Funding Group today to discuss your promissory note and find out what options may be available.